Introduction

When I first started managing my finances as a new parent, I thought the key to staying on track was to log every expense meticulously. It felt empowering at first—like I had total control over where my money was going. But the process soon became tedious, particularly when going through and categorising transactions that modern banking apps couldn’t automatically sort.

The effort paid off, though. Reviewing all my expenses revealed patterns I hadn’t noticed before—small gadgets I barely used, toys for my son that quickly lost their appeal, and a mountain of subscriptions I was hardly using. The insights were invaluable and made me rethink how I spent my money.

So, should you track every penny? Based on my experience, here’s a look at the pros and cons, along with tips to help you decide if it’s right for you.

The Pros of Tracking Every Penny

1. Awareness Is Empowering

The first time I reviewed my expenses in detail, I realised how much I was spending on small, seemingly insignificant purchases. Gadgets, toys for my son, and occasional impulse buys added up to hundreds of dollars over a month.

For example, I found that while I enjoyed my subscriptions—Netflix, Disney+, Amazon Prime, Stan, Xbox Game Pass, and Audible—I was only using them occasionally. They were costing me far more than I realised. The same went for my gym membership; despite good intentions, I rarely went, and the cost was difficult to justify.

What I Gained:

This awareness made me think more critically about my spending habits. It wasn’t about guilt—it was about understanding the true value of what I was paying for.

What You Can Do:

Track your expenses for a month and review categories where spending tends to creep up, like subscriptions or impulse buys.

2. It Helps You Set Clear Priorities

Tracking every penny showed me where my money was going and helped me align spending with what mattered most. For example, I realised I valued family outings, like trips to the zoo or a beach weekend, more than eating out or takeaway coffee at work.

I also found that I could save by drinking the free, and surprisingly good, coffee available at work instead of grabbing a $4 cup every morning. Small changes like these freed up money for experiences that brought lasting joy.

What I Gained:

Once I knew my priorities, it was easier to redirect spending toward the things that truly mattered, like family experiences or long-term savings goals.

What You Can Do:

Use your tracking data to identify what adds value to your life and cut back on things that don’t.

The Cons of Tracking Every Penny

1. It Can Be Time-Consuming

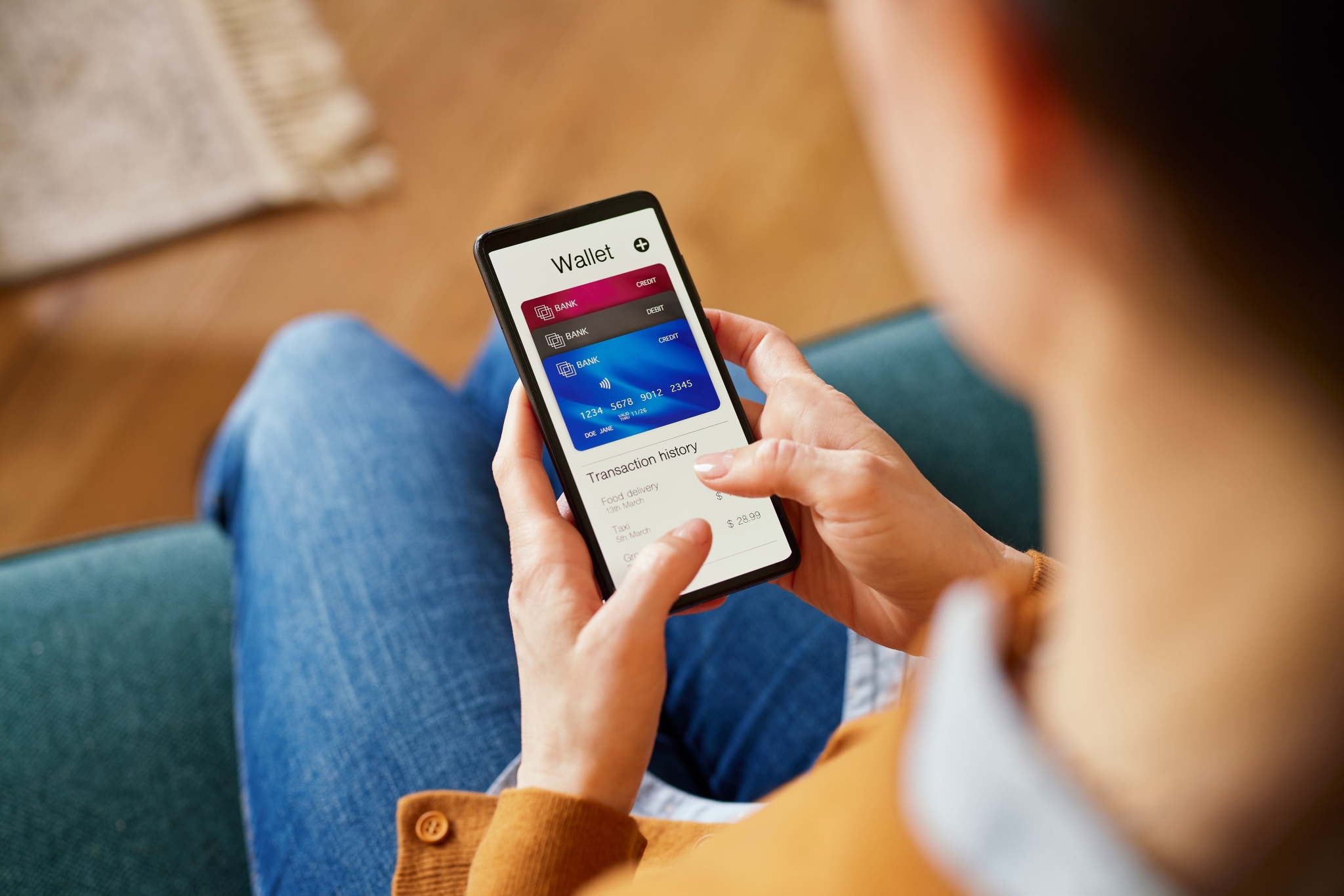

Modern banking apps have made tracking easier, but it’s still not completely effortless. While apps often categorise many transactions, I found myself going through each one to double-check accuracy and categorise things like cash spending.

For example, categorising takeaway snacks, small purchases, or irregular expenses took more time than expected. While the insights were valuable, the process sometimes felt like an added chore.

What I Learned:

You don’t need to track every penny forever. Start with a detailed review for a few months to spot patterns, then scale back to only tracking key categories like subscriptions or dining out.

What You Can Do:

Focus on high-impact categories where you can save the most. If you use a banking app, take advantage of its automatic categorisation and add manual reviews for uncategorised transactions.

2. It Can Lead to Stress or Overthinking

While tracking every expense brought clarity, it also made me overthink small indulgences. For example, I felt guilty about treating myself to a coffee or a small toy for my son, even when it was within my budget.

What I Learned:

Budgeting should feel empowering, not restrictive. Allowing space for discretionary spending—without guilt—helped me strike a balance between saving and enjoying life.

What You Can Do:

Set aside a “fun money” budget for guilt-free indulgences. Knowing it’s already accounted for makes spending on small joys feel intentional rather than impulsive.

Finding Balance: Alternatives to Detailed Tracking

If tracking every penny feels unsustainable, there are simpler approaches that can still help you stay in control:

-

Track by Category:

Instead of logging every transaction, focus on broad categories like dining out, entertainment, or subscriptions. Most banking apps in Australia provide automatic spending summaries, and similar tools are available in other countries. -

Use a Percentage-Based Approach:

Frameworks like the 50/30/20 rule simplify budgeting by dividing your income into needs, wants, and savings. -

Automate Bills and Savings:

Set up automatic transfers to savings accounts and direct debits for bills. This ensures essentials are covered without constant monitoring.

Conclusion

Tracking every penny can be a powerful way to gain control over your finances, but it’s not the only approach. For me, the process revealed valuable insights into my spending habits, from unnecessary subscriptions to the hidden costs of convenience.

The key is finding a system that works for you—whether it’s detailed tracking, a category-based approach, or automation. By focusing on your priorities and making mindful adjustments, you can create a budgeting system that feels less like a chore and more like a tool for intentional living.

Remember, budgeting isn’t about perfection—it’s about progress. With each thoughtful decision, you’re taking a step toward a life aligned with your values and goals.